Currency risk in portfolios

Currency movements can affect investing outcomes. Investors owning overseas assets therefore are naturally concerned about what to do with this risk. The two options are to accept currency risk, or transfer it to another party willing to accept it, for a cost. The decision of what to do with currency exposure differs based on the role of the asset class in the portfolio.

So far in 2025, most major currencies have appreciated against the dollar, with AUD, CAD, GBP, JPY and EUR all up somewhere between 5-12% YTD[1]. Naturally, this has brought currencies movements back into sharp focus for globally diversified investors.

Currency markets are notoriously difficult to profit from consistently. In fact, most strategies are beaten by those simply following a random walk[2]. Websites allowing individuals to trade things such as currency pairs often include a clear warning to state that most traders lose money[3].

Therefore, accepting that one cannot predict the direction of currency movements, the only reason one might choose to accept or transfer currency risk to another is if it is expected to materially affect the ability for an investment to perform its role (such as limiting the defensive assets to be defensive in nature). This is explored in more detail below.

Component parts of an investment portfolio

Your portfolio is broadly split into two distinct parts: growth assets and defensive assets. The former is designed to be the core return engine, and the latter to dampen volatility and provide protection during times of economic turmoil.

Defensive Assets

The importance of protecting from currency exposure in defensive assets

For defensive assets such as high-quality bonds, currency risk is significantly greater than the risk of the underlying asset itself, therefore transferring currency risk in this part of the portfolio is key. This is achieved through a technique called ‘currency hedging’ within the underlying funds, which essentially ensures that any currency movements are removed from the returns achieved. The graphic below demonstrates the material reduction in risk through the process of hedging currency exposure of overseas bonds.

Data source: Payden Global Government Bond Index, iShares Global Government Bond ETF, Vanguard Global Stock Index. Period: 01/04/2011 - 31/05/2025. Returns stated in GBP.

Defensive assets are intended to provide stability, and exposure to currency fluctuations can undermine their role. Despite the additional cost associated with hedging, the marked reduction in volatility justifies this approach, ensuring defensive assets meet their objectives, particularly during market downturns.

Growth Assets

Deciding what to do with currency exposure is less obvious for growth assets

In the context of growth assets, typically comprising stocks, the decision to hedge currency risk is more nuanced. Unlike with defensive assets, hedging currency within the growth assets does not consistently reduce overall risk. Hedging simply reverses the pattern of the impact of currency movements.

Historical correlations between currency movements and global stock markets have been inconsistent across markets, making outcomes unpredictable, and the volatility of currency markets and stock markets typically similar over time.

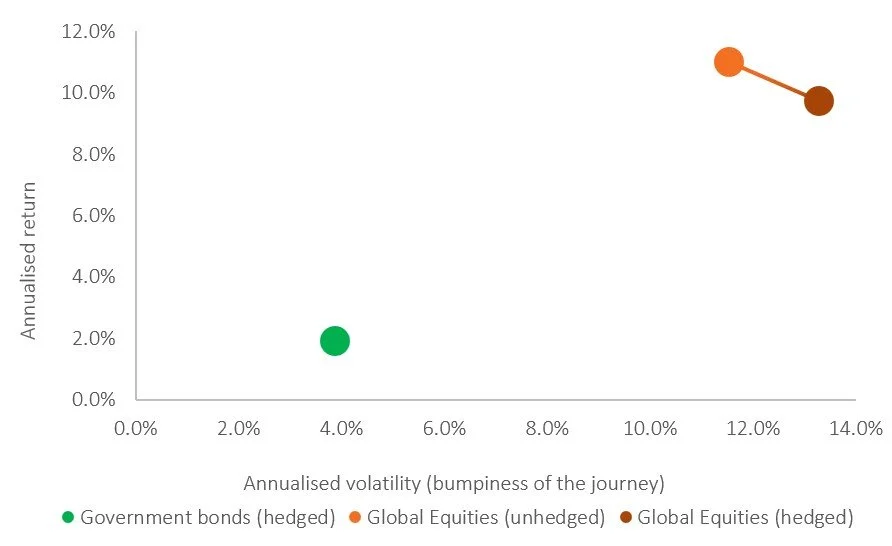

Figure 2: Comparing currency hedged and unhedged equities | Data source: Payden Global Government Bond Index, iShares MSCI World GBP Hedged ETF, Vanguard Global Stock Index. Period: 01/04/2011 - 31/05/2025. Returns stated in GBP.

Retaining unhedged exposures in growth assets avoids the cost of hedging. As a more nuanced point, during periods of high local inflation, the local currency typically depreciates accordingly. This then means that overseas assets, when priced in one’s local currency, buy more of the depreciated currency. In short, an unhedged overseas stocks exposure might (but is not guaranteed to!) provide a long-term protection against high local inflation. It is also true that a lack of currency hedged products across asset classes may pose additional challenges for investors.

On balance, therefore, leaving the growth asset currency exposures unhedged makes good sense.

Three key considerations when it comes to dealing with currency risk

Protecting against currency exposure in defensive assets is an effective way to reduce volatility.

In growth assets, hedging currency exposure is neither expected to enhance returns nor reduce volatility, and may increase complexity and costs.

Avoid predicting currency markets – few, if any, are able to profit from doing so reliably.

Do you have concerns about currency risk within your portfolio? If so, please feel free to get in touch via the link below.

[1] Source: Koyfin as at 12/06/2025. All rights reserved.

[2] E.g. Moosa, I. (2013). Why is it so difficult to outperform the random walk in exchange rate forecasting? Applied Economics, 45(23), 3340–3346. https://doi.org/10.1080/00036846.2012.709605

[3] See ig.com, trading212.com, and etoro.com as examples