The Riches Report Blog

The Client Diary: Week of 14th July 2026

This week’s conversations could not have been more different on the surface. One client was mapping out gifting strategies for children and grandchildren, another was travelling the world while navigating a multi-million pound inheritance tax challenge, and another was simply trying to ensure a loved one’s care is funded with dignity.

But beneath it all, the same themes kept surfacing.

Three, in particular, stood out.

The Client Diary – Week of 6th July 2026

One of the most fascinating aspects of financial planning is that, eventually, every conversation becomes a family conversation.

This week I found myself speaking with two very different families, yet both were wrestling with exactly the same question

Bonds: the basics

This is the first note in my new Back to basics series: “Bonds: the basics.”

This new collection of articles is designed to explain some of the core concepts in investing in a clear and accessible way. The aim is to provide useful material that support clients’ understanding of important investment principles.

This first note focuses on bonds - what they are, how they work, why they are often described as “fixed income”, as well as the types of bonds included in sensible investment portfolios.

Investing at all-time market highs

Stock markets reaching all-time highs can feel both reassuring and unsettling. On the one hand, rising markets are a sign that long-term investors are being rewarded for taking on the risks that come with stock ownership. On the other, new highs can prompt the understandable question: is now the wrong time to invest, or the right time to take some money off the table?

The Client Diary: Week of 8th June 2026

Four meetings this week, spanning a long-standing clients’ annual review, a new prospect discovery, a follow-up with a specialist lender, and a conversation with Vanguard around adviser development. They could not have looked more different on the calendar. One centered on long-term legacy and family wealth, another on an entrepreneur still very much in building mode, one on the mechanics of borrowing, and one on how we as advisers improve what we do to better help our clients.

Your adviser as your investment coach - Part 7

A key level of value that an adviser delivers is undertaking some of the menial, yet highly valuable, administrative functions. One such example being tax planning in a controlled manner, avoiding as little time out of the market as possible. We all hate paperwork, so let someone else take care of it!

SpaceX IPO through a systematic lens

An Initial Public Offering (IPO) represents the point that a company decides to ‘go public’ by listing its shares on the stock market, allowing investors to become part owners of the company itself. The upcoming SpaceX IPO has attracted significant attention – particularly across broadsheets and financial media – due to the imminent stock market listing, expecting to make it the largest company ever to list on the stock market. Anthropic Labs and OpenAI are expected to follow later this year.

The Client Diary: Week of 1st June 2026

Five meetings this week, spread across a prospect discovery, a couple of onboarding check-ins, an annual review, and a long-standing client check-in over coffee. On the surface, very different conversations — a business sale generating life-changing wealth, a retiree navigating her husband's care, a newly-retired couple finding their feet, and a prospect arriving with a perfectly good financial life but no real map of it. Underneath, though, four themes kept pulling the conversations in the same direction.

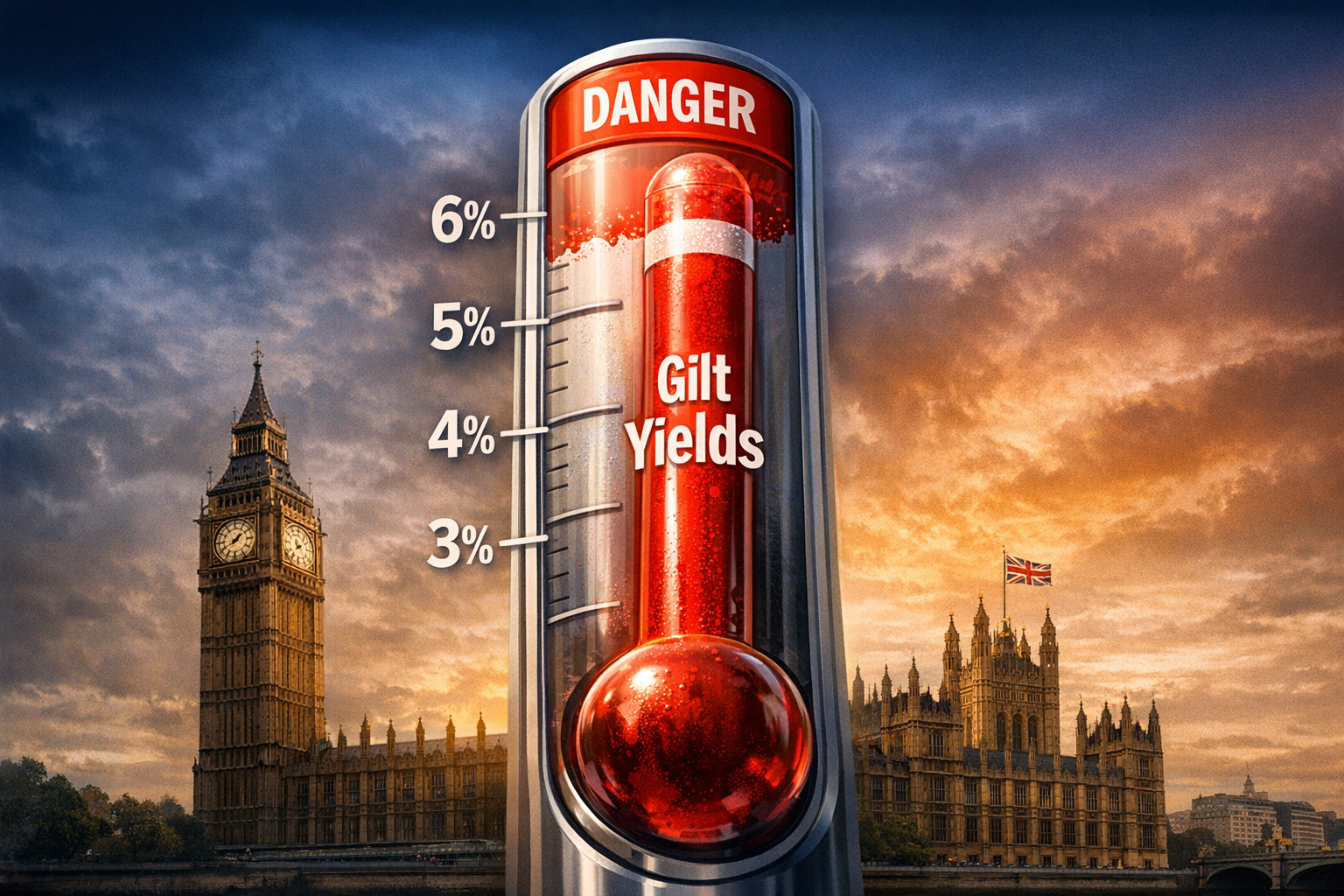

Gilt yields and governments

Those paying attention to the news in recent weeks may have noticed some alarming headlines about UK government borrowing costs. UK government bond (‘gilt’) yields, readers were told, were surging. Then, just as quickly, they were falling again. It can all feel rather unsettling, especially when it appears to be tangled up with political events close to home.

The Client Diary: Week of 11th May 2026

Two meetings stood out this week — a home visit to a long-standing client approaching a milestone birthday, and an annual planning session with one of the most financially self-aware people I work with. Very different circumstances, different parts of the country, different chapters of life. And yet by the end of the week, I found myself turning over the same three ideas. Here they are.

Your adviser as your investment coach-Part 6

Your adviser plays an important role as your investment coach. This series of short notes explores six ways a good adviser can add real value to a client’s investment programme.

The Client Diary: Week of 4th May 2026

Four days, five meetings, and an investment committee thrown in for good measure. Two annual planning meetings with long-established clients confirmed, once again, what the numbers have been saying for a while. A brief check-in with a client in the middle of a complex structural wind-down. A catch-up with a younger client navigating significant personal change. And a morning spent with our investment philosophy partners reviewing the portfolios in proper detail. Between them, three themes kept resurfacing.

The Client Diary: Week of 27th April 2026

Three meetings across four days — a financially sophisticated business owner who arrived with a sprawling portfolio and left with a consolidation plan and a clearer view of the estate she wants to build for her family; an 80-year-old at a financial crossroads, with a flat to sell, a generous instinct, and a quiet but serious question about care costs; and a long-standing client who arrived with the low-level dread that he might be running out of money, and left with something he had not expected to feel: relief. Between them, they covered a remarkable amount of ground. Here are the three themes that stayed with me.

Your adviser as your investment coach-Part 5

Your adviser plays a key role as your investment coach. This series of short notes will explore six ways that a good adviser will bring true value to a client’s investment programme.

The Client Diary: Week of 20th April 2026

Three very different meetings this week — a deep retirement implementation session with a couple on the cusp of drawing down, an advanced planning conversation with a tech entrepreneur wrestling with crypto and corporate cash, and a coffee with a prospect who arrived frustrated and left, hopefully, with a clearer picture. Between them, they covered a remarkable amount of ground. Here are the themes that stuck with me.

The Client Diary: Week of 13th April 2026

Some weeks in financial planning feel fairly routine — portfolio reviews, a bit of tax housekeeping, the usual quarterly check-in. And then there are weeks like this one.

Your adviser as your investment coach - Part 4

Your adviser plays a key role as your investment coach. This series of short notes will explore six ways that a good adviser will bring true value to a client’s investment programme.

The Client Diary — Week Of 7 April 2026

A week of annual planning meetings. Two very different clients. One unmistakable theme running through both.

Your adviser as your investment coach - Part 3

Your adviser plays a key role as your investment coach. This series of short notes will explore six ways that a good adviser will bring true value to a client’s investment programme.

Your adviser as your investment coach - Part 2

You adviser plays a key role as your investment coach. This series of short notes will explore six ways that a good adviser will bring true value to a client’s investment programme.