Gilt yields and governments

Those paying attention to the news in recent weeks may have noticed some alarming headlines about UK government borrowing costs. UK government bond (‘gilt’) yields, readers were told, were surging. Then, just as quickly, they were falling again. It can all feel rather unsettling, especially when it appears to be tangled up with political events close to home.

Gilt yields move around a lot - this is not new. They are driven by a great many things at once, and do have direct impacts on individuals (eg borrowing costs, savings rates). However, short-term movements provide limited information for long-term, globally diversified investors.

Gilts: the basics

A gilt is simply an IOU with the UK government. When the government needs to borrow money, it issues gilts. Investors who buy them are lending money to the government in return for a fixed series of interest payments (the coupon) and the return of their original sum when the loan matures.

The yield on a gilt is the annual return an investor receives if they buy it at today's market price and hold it to maturity. Yield and price always move in opposite directions, like a seesaw. When investors are happy to accept a lower return for lending to the government, yields fall and prices rise. When they demand more compensation, yields rise and prices fall.

Politics and investing

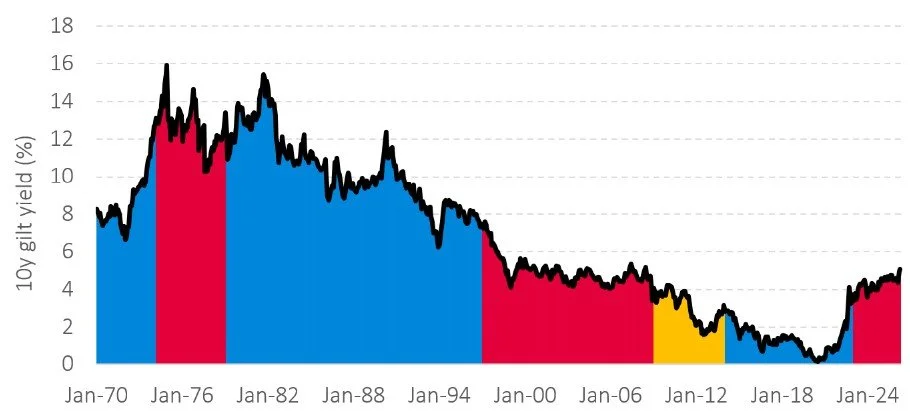

The figure below shows UK gilt yields over the longer term. Yields spent much of the past decade at historically low levels, and at times close to zero, before rising sharply from late 2021 onwards. That longer history contains different governments, many (and mini!) budgets, and many moments of political upheaval. Yields moved through all of them, in both directions.

Figure 1: Gilt yields over time based on UK political party in power.

Source: Albion Strategic Consulting. Data source: Bank of England. Using 10y nominal monthly spot curve, Jan-70 to Apr-26. Blue = Conservative, red = labour, yellow = coalition.

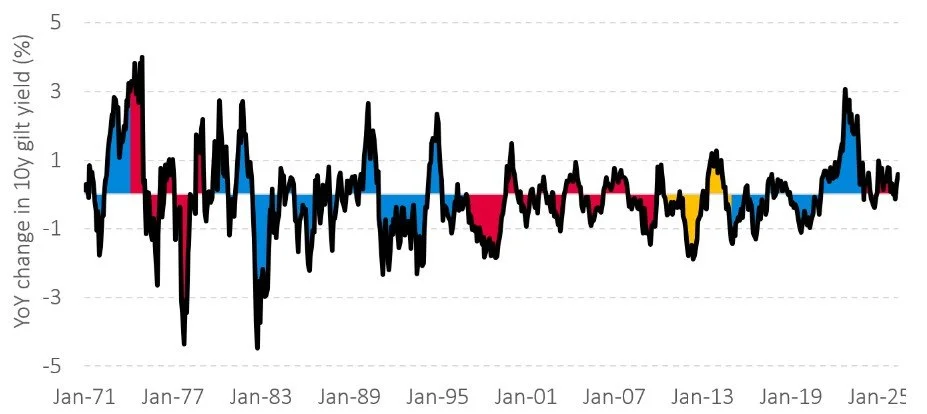

The figure below shows the same data, but instead gives a view of the year-on-year change in the level of the yield. This gives a sense of how large and how frequent these movements can be. Like the figure above, it is not possible to find a reliable pattern.

Figure 2: 1-year change in gilt yields based on UK political party in power.

Source: Albion Strategic Consulting. Data source: Bank of England. Using 10y nominal monthly spot curve, Jan-70 to Apr-26. Blue = Conservative, red = labour, yellow = coalition.

Avoid trying to outguess markets

Gilt yields are shaped by a large number of forces, all pushing and pulling at the same time. The Bank of England’s base rate (and what markets expect it to do next), inflation expectations, geopolitics, commodity prices, and government borrowing plans will, amongst a long list of other matters, all affect gilt prices.

Political events can, at times, nudge some of these factors. A significant fiscal announcement, for example, may affect confidence in the government's borrowing plans at the margin. But they are only ever one input among many, and their impact is rarely as lasting as the headlines suggest.

If the direction and magnitude of price movements were truly knowable, investors would already have acted on that information and current yields would already reflect it. Markets aggregate the views of enormous numbers of participants. The scope for any one person, government, or institution to predict the direction of yields with any reliability is very limited.

Even the professionals struggle to second guess gilt markets. In the ten years to December 2025, fewer than 10% of professional fund managers in the UK gilt space managed to beat the wider gilt market.

What this means for long-term investors

The bond allocation in a client portfolio is there to provide stability relative to equities. It is not designed to make directional bets on yields. Short-term movements in yields, in either direction, are a normal part of owning bonds.

The portfolios we recommend also includes a globally diversified bond allocation, mitigating the impact of movements in one specific market.

It is worth remembering that today's yields are materially higher than the near-zero levels of just a few years ago. That is, in fact, good news for longer-term investors. Those holding shorter-dated bonds are likely to have already eaten through the pain of the price falls seen in 2022.

The same logic applies in reverse. Falling yields feels reassuring as it brings a rise in price, but they gradually reduce the future return available from bonds. Neither direction is straightforwardly good or bad.

It can be tempting, when yields are moving and headlines sensationalise events, to draw a direct link between political events and your investments. In reality, no one knows with any reliability where yields will be in future.

Sensible investing requires an understanding that the noise of markets is part of the experience of investing. Political predictions are best left out of the investment portfolio construction process.

If you would like to understand more about the role bonds (gilts) could play in your portfolio or even whether they should be included at all in your own circumstances please feel free to get in touch via the link below.