SpaceX IPO through a systematic lens

An Initial Public Offering (IPO) represents the point that a company decides to ‘go public’ by listing its shares on the stock market, allowing investors to become part owners of the company itself. The upcoming SpaceX IPO has attracted significant attention – particularly across broadsheets and financial media – due to the imminent stock market listing, expecting to make it the largest company ever to list on the stock market. Anthropic Labs and OpenAI are expected to follow later this year.

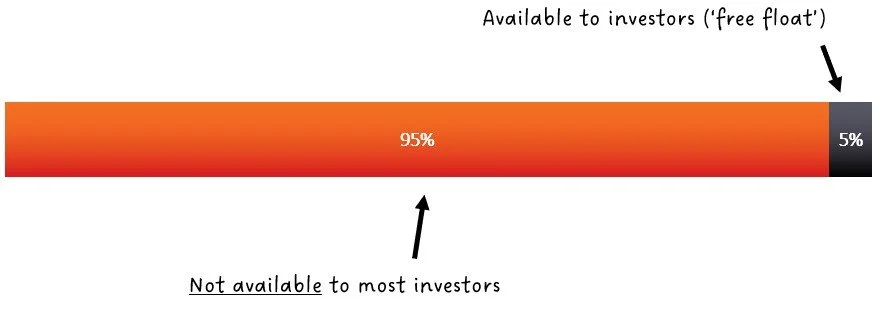

While a large IPO may appear immediately significant, its actual impact on an investment portfolio depends on several factors, including how much of the company is available for public trading (free float), the eligibility requirements of index providers, and how fund managers approach IPOs. In practice, even very large companies may initially float only a small proportion of their shares, meaning that the amount available to investors at the point of listing can be relatively limited. By way of example, SpaceX is expected to float in the region of 5% of its total company.

In simple terms, the freely floated stocks in a company represent what investors can actually buy. Some companies list the vast majority of stock, meaning ownership is largely public. Microsoft is one such example. Others may choose to list only a small proportion, with the remainder being owned by others such as founders, employees, or other stakeholders.

The distinction is important because most market indices – and the funds that track them – weight companies based on free float adjusted market capitalisation. As a result, a company may have a very large market capitalisation (i.e. its total size), but if only a small proportion of shares are freely available its weight within an index, and therefore in portfolios, can be materially smaller. The figure below illustrates the phenomenon.

Figure 1: Illustration of free float shares compared to total outstanding (5% float)

Source: Albion Strategic Consulting

It is worth noting that this is not the first time such a phenomenon has occurred. In 2019, Saudi Aramco floated less than 2% of its shares, and its valuation meant it was the biggest listed company in the world. However, with the small quantity of shares floated, few investors would see this stock appear in the portfolio’s top stock holdings.

It is also important to recognise that this effect can evolve over time. IPOs may include “lock-up” provisions, which restrict existing shareholders from selling their holdings for a defined period after public listing. As these restrictions expire, additional shares may come to market, gradually increasing the free float and, in turn, the company’s weight in indices and portfolios.

Index inclusion is also not immediate or guaranteed. Major index providers apply specific criteria that determine both eligibility and timing of entry. In some cases, index providers may accelerate inclusion for large companies, but weighting is still typically based on free float, which can limit initial portfolio impact. These can include:

· Minimum total and float-adjusted market capitalisation (e.g. >$10bn)

· Minimum free float (e.g. 10% of company, or greater than $2bn)

Other fund managers may operate differently and may have other more flexible rules for inclusion. In practice, some strategies delay investment, reflecting the view that there can be a lack of price discovery soon after listing.

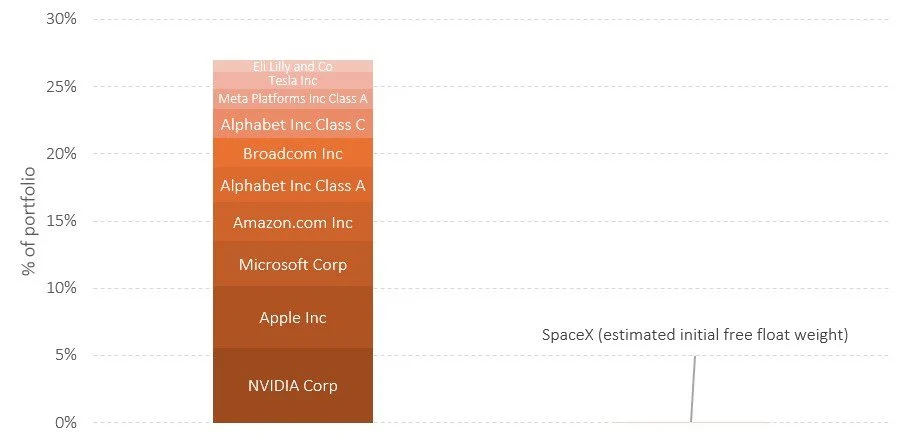

Figure 2: % in top 10 holdings in a market index fund, and initial expected free float size of SpaceX

Source: Albion Strategic Consulting. For illustrative and example purposes only. SpaceX approximation based on expected initial free float weight of around 0.1% (several sources estimate the initial listing to be around $75bn. The US stock market is currently over $75T).

It is worth noting that in the portfolios I typically recommend, as is the case for all systematic investors, a starting point is the view that market prices incorporate all available information quickly enough that persistent pricing inefficiencies are difficult to identify and exploit. Few professionals can do so. Tilting towards well documented risk factors such as value and small cap will result in an exposure to IPO allocations that will typically differ from that of a pure market index.

The exact exposure will depend on the company’s characteristics. If SpaceX or any other company trades as a growth company, a value tilt would likely lead to an underweight relative to the market. Conversely, if it exhibits value-like characteristics (trading at a lower price relative to fundamentals) it could receive a relatively higher allocation.

Over time, this divergence may become more pronounced. If the company evolves, potentially through increased free float size, high investor sentiment, or a combination of both, its characteristics may shift (consideration of both value and size). This, in turn, could lead to greater variation. Ultimately, the stock market will price in any new information quickly.

While the SpaceX, Anthropic and OpenAI IPOs may seem significant in headline terms, the impact on portfolios may well be modest initially. Limited free float plays a major part, index inclusion is governed by rules and thresholds, and systematic managers are not necessarily forced buyers at IPO.

Over time, as additional shares become available and valuations evolve, the influence of such companies may increase, but this process may well occur gradually rather than immediately.

My own firms Investment Committee will continue to stay close to the issue and developments before, during and after the listing. Do feel free to get in touch with your own thoughts.