Your adviser as your investment coach - Part 3

Your adviser plays a key role as your investment coach. This series of short notes will explore six ways that a good adviser will bring true value to a client’s investment programme.

· Value level 1: Establish your guiding principles

· Value level 2: Build a robust portfolio for all seasons

· Value level 3: Maintain the efficacy of the portfolio and avoid fads

· Value level 4: Providing support and guidance along the way

· Value level 5: Instilling the fortitude and discipline to rebalance

· Value level 6: Doing the boring stuff

This note delves into the second of these value levels: Build a robust portfolio for all seasons.

Value level 2: Build a robust portfolio for all seasons

Now that an investor has a focus on how to invest, the next step in the investment process is to decide what to invest in. The choice is vast, but the solution – provided you have an astute adviser at the helm – can be reduced down to an elegantly simple set of risk choices. The returns that these risks should deliver are captured using institutional quality, low cost funds that seek to deliver the return of each market risk as effectively as possible (rather than trying to beat the market, which is a futile pursuit according to the evidence).

The first and primary decision to make is to decide how much to invest in growth assets, such as stocks, and how much to invest in defensive assets, such as high-quality bonds that should offer protection from large stock market falls. The overall mix of investments is known in the industry jargon as ‘asset allocation’. Your adviser will help by determining the appropriate asset allocation based on a deep understanding of your situation.

A good adviser will have a disciplined screening programme that will ensure that each type of investment (asset class) is worthy of its place in the portfolio. Our Investment Committee holds this responsibility, and adopts a framework through which it argues reasons for and against a wide range of asset classes’ inclusion in investment portfolios.

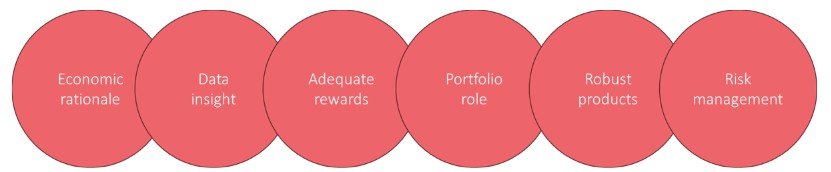

Details of the Investment Committee’s asset class review criteria are provided below.

Criterion 1: Economic rationale for returns

Be clear where the returns are meant to come from. This comes through a proper understanding of underlying risks.

Criterion 2: Useful data insight

Check there is enough good, reliable data to understand how an asset class behaves.

Criterion 3: Adequate rewards for the risks taken

Make sure the expected return is worth the extra risk taken on compared with other options. Extra risk should only be taken on if there is an expectation that one will be compensated for it.

Criterion 4: Contribution at a portfolio level

Look at what the asset class does to the whole portfolio. Some may be expected to provide protection during poorer markets (e.g. high-quality bonds). Others may be included as core return drivers (e.g. global stock markets). Regardless, an asset class’ role should be clear and defined. Remember that to add something into a portfolio, something must be taken out.

Criterion 5: Robust products to access characteristics through

Make sure there’s a simple, low-cost, liquid way to invest in the asset class. It becomes more difficult to argue the case for inclusion if the only available products are expensive, hard to access or excessively complex.

Criterion 6: Risk management demands

Think about how hard it is to manage properly over time (monitoring, controls, expertise needed).

Figure 1: Asset class review framework | Source: Albion Strategic Consulting

As the late David Swensen stated:

By understanding and articulating the role played by each asset class, investors avoid making allocations based on the fashion of the day.

The thing to remember is that in investing there is no single perfect solution to building a portfolio. Success lies in a sensible structure with the long-term attributes of each portfolio building block contributing positively to the overall portfolio, and the recognition that in the short-term, some elements of the portfolio will do well and other elements less so. This is expected and by design.

If you have questions about the structure of your portfolio please feel free to get in touch via the link below.