Your adviser as your investment coach-Part 6

Your adviser as your investment coach

Your adviser plays an important role as your investment coach. This series of short notes explores six ways a good adviser can add real value to a client’s investment programme.

· Value level 1: Establish your guiding principles

· Value level 2: Build a robust portfolio for all seasons

· Value level 3: Maintain the efficacy of the portfolio and avoid fads

· Value level 4: Providing support and guidance along the way

· Value level 5: Instilling the fortitude and discipline to rebalance

· Value level 6: Doing the boring stuff

This note looks at the fifth of these value levels: Instilling the fortitude and discipline to rebalance.

Value level 5: Instilling the fortitude and discipline to rebalance

As part of the financial planning process, you will have spent a good deal of time with your adviser discussing ‘risk’ and what it means for you. Quite right too, because this is not something to get wrong at the outset of your journey. The ‘right’ level of risk in a portfolio depends on how comfortable you are with the trade-off between upside gains and downside pain (your risk tolerance), how much risk you need to take to achieve your goals (your risk need), and your financial ability to absorb losses without derailing those goals (your capacity for loss). Your investment experience and level of interest can also play a part.

Once you and your adviser have worked through these issues carefully, it makes sense to keep your portfolio’s level of risk broadly consistent over time, unless your circumstances change materially. If they do, this should be discussed in one of your regular review meetings.

As your adviser will have explained, growth assets such as equities (stocks) offer higher expected long-term returns than defensive assets such as high-quality, short-dated bonds. They also come with a much wider range of outcomes. Over time, the weightings of these assets (and of subcomponents such as developed and emerging market equities, property and index-linked bonds) will shift as markets move.

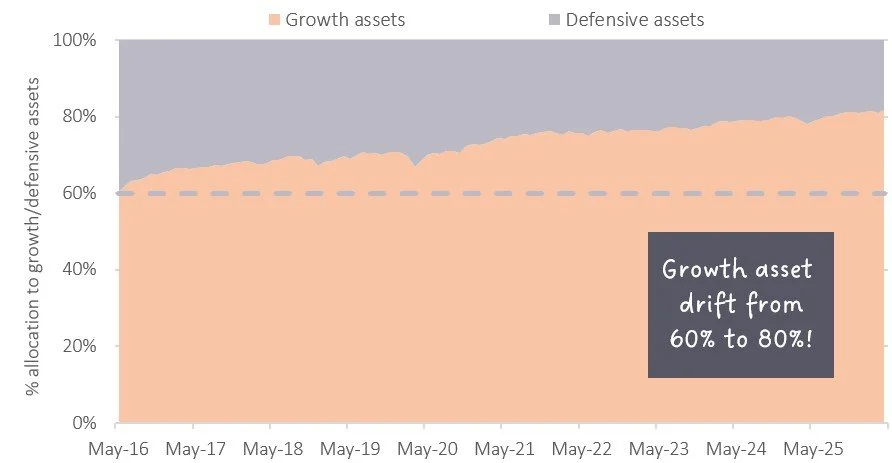

Left unrebalanced, portfolios can drift away from the level of risk that makes sense for you. As the chart below shows, a portfolio made up of 60% global equities (‘growth assets’) and 40% short-dated global bonds (‘defensive assets’) would have drifted to over 80% in growth assets over the past 10 years. That is why your adviser will have talked to you about rebalancing: the relatively simple, disciplined process of realigning your portfolio back to, or close to, the original level of risk agreed with you.

Figure 1: Drift in growth/defensive asset exposure of 60/40 portfolio from May-16 to Apr-26

Source: Albion Strategic Consulting. Data source: Albion World Stock Market Index and Albion Global Short Bond Index (0-5, GBP), before inflation.

Unfortunately, humans do not always make good investors. At times, rebalancing can feel emotionally difficult. Equities may have performed sparklingly, and your adviser may recommend selling some of them to buy those duller bonds that may have been holding back returns. A portfolio left overweight in equities, however, is likely to suffer bigger falls in value than one that is regularly rebalanced. Those falls may become too much to bear, prompting an investor to abandon the strategy altogether, which is not a good idea.

Equally, when equity markets have fallen sharply, your adviser may recommend selling some of your reassuringly safe bonds to buy more of the very equities that have just hurt your portfolio and could yet fall further.

The Great Financial Crisis, which began in late 2007 and reached its low point in early 2009, is a good example. A portfolio holding 60% in stocks and 40% in short-dated, high-quality bonds would have drifted to well below 50% in stocks between November 2007 and the end of February 2009, the trough of the market crash.

Under that kind of emotional pressure, many investors would have been tempted to sell even more stocks. It was a very worrying time. A good adviser would have been recommending the opposite: trimming the now overweight bond allocation and buying stocks to restore the portfolio to its intended level of risk. At moments like these, rebalancing may feel uncomfortable, but it remains essential. In this instance, the market rebounded strongly.

Rebalancing may sometimes add a little to returns, but there are no guarantees. A good adviser will, perhaps rather boringly but quite correctly, remind you that rebalancing is primarily about keeping your risk level appropriate for you, not about chasing higher returns. As the late David Swensen, former CIO of Yale University’s Endowment and one of the world’s most respected institutional investors, put it:

‘The fundamental purpose of rebalancing lies in controlling risk, not enhancing returns. Rebalancing trades keep portfolios at long-term policy targets by reversing deviations resulting from asset class performance differentials. Disciplined rebalancing activity requires a strong stomach and serious staying power.’

Especially in periods of market stress, rebalancing is emotionally hard. Fortunately, putting a systematic rebalancing process in place that triggers a rebalance - either at regular intervals and/or when the mix of growth and defensive assets has moved materially because of market movements – can help to take some of the emotion out of the decision. The rebalancing process will have been discussed with you when your portfolio was set up. Your adviser can monitor this for you and work out the trades needed to bring your portfolio back to where it should be. Leave that to them.

Your job is simply to stay disciplined, be brave and to trust their advice.

If you are not receiving regular reviews during which rebalancing is discussed or have concerns about your current portfolios asset allocation please feel free to get in touch.